Contrary Research Rundown #129

Is CoreWeave a canary in the coal mine for AI? Plus, new memos on Abridge, Crusoe, and more

Join Contrary and Ramp in NYC on April 3rd for Undo. Undo. Redo. - a celebration of both design failures and triumphs. This lightning-talk style event for senior designers will feature unabridged stories from Contrary, Ramp, Anthropic, and Notion.

Register here for the chance to join!

Research Rundown

Yesterday, we saw the first IPO of a truly AI-centric company amidst a seemingly endless demand for AI-everything. CoreWeave went public at $39, ending its first day at $40, with an $18 billion market cap, below the $35 billion where the stock had initially priced. In a world of massive of private and public capital being thrown at businesses across the hardware, infrastructure, and application layers of AI it raises a question of why this IPO didn’t reflect the exuberance people are feeling about AI?

First, it’s important to understand that many view CoreWeave as having a fundamentally flawed business which has been shaped as a response to a fervent moment in AI.

Second, CoreWeave’s success is tied directly to an overarching question about the durability of AI demand. And people are feeling cautiously nervous about that question.

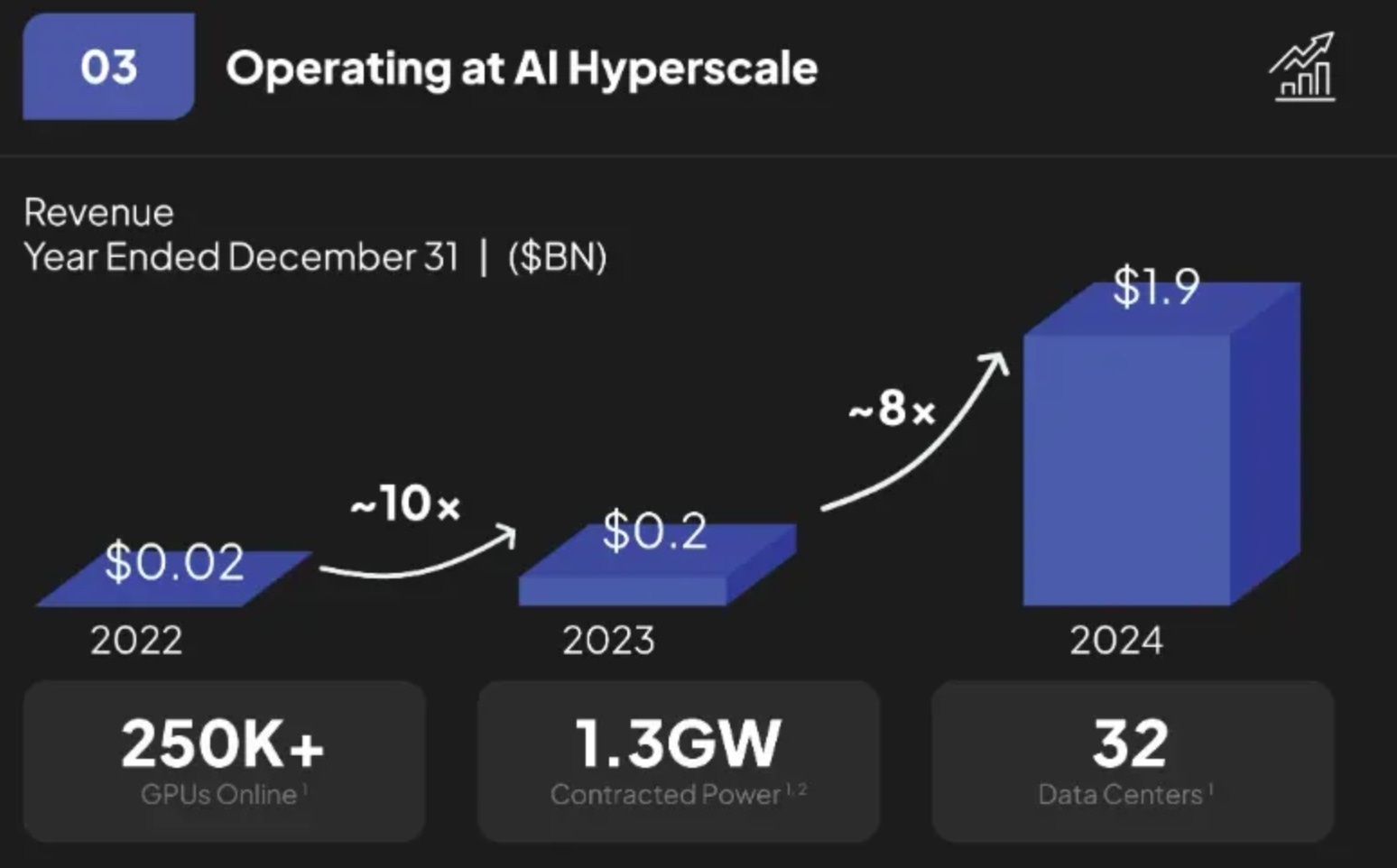

To understand CoreWeave’s business, you can look back at the history we unpacked in our memo here. The origins of the business began in 2016 when the co-founders began buying GPUs for crypto mining. Over time, the team began renting GPUs out for crypto mining as well. They pivoted to cloud infrastructure in 2019, and suddenly grew 271% within the first three months after the pivot. Fast forward to the spark that was ChatGPT and the race was on. From 2022 to 2024 the company grew from $20 million to $1.9 billion in revenue.

At its core, CoreWeave’s business is buying Nvidia GPUs and renting them out for AI-specific workloads. CoreWeave’s biggest customer? Microsoft. Most companies look to diversify their customer base ahead of an IPO, but CoreWeave has taken a real contrarian approach and actually seen its revenue concentration increase. Microsoft, as a percentage of CoreWeave’s revenue, has increased from 35% in 2023 to 62% in 2024.

In order to service customers, CoreWeave has an incredibly CapEx-heavy business model. Because CoreWeave’s core value proposition is providing access to cutting edge GPUs for AI workloads, it means that every time the company spends money on hardware, it starts the clock on when that hardware will become obsolete. As a result, CapEx represents 400% of CoreWeave’s revenue.

With the massive capital expenditures on hardware comes a lot of depreciation. Because the company is so focused on the cutting edge, its assets depreciate quickly. One report ahead of the IPO expressed some raised eyebrows about where depreciation is accounted for. While clearly a cost of doing business, CoreWeave indicates ~75% gross margins. But adding depreciation back into COGS would bring those margins down to ~30%.

The takeaway is that you have a business with a complex financial profile that is very much held up by exorbitant demand for computing resources. Which brings us to the second question of CoreWeave’s business, and what it means for the durability of AI. One question you might be asking is why is Microsoft expected to spend $10 billion on CoreWeave by the end of the decade if Microsoft is also set to spend $80 billion on AI data centers this year alone?

In an earnings call in November 2024, Microsoft explained how it was struggling “to have enough GPU servers online to meet customer demand.” CoreWeave represents one way to augment that demand. But at the same time, you have Microsoft walking away from some new data center projects, as one report indicates that the move “points to data center oversupply relative to its current demand forecast.”

So the question is whether there is an oversupply or undersupply of computing resources for what AI demand will look like at steady state? And, more specifically, is the current rate of AI infrastructure spend a bubble? Or sustainable? While CoreWeave’s business is dependent on these heightened levels of spend being the status quo, the behavior of the founders and investors doesn’t seem to indicate that they buy into that. Ahead of the IPO, CoreWeave’s co-founders sold nearly $500 million of their stake.

Some argue that CoreWeave isn’t indicative of the broader AI market because of all these aspects of its business — it’s built on debt, high CapEx, massive depreciation, not to mention the more than $5 billion in cash the company burned, even on $2.8 billion of revenue. All fair points. But fundamentally, CoreWeave’s business is tied directly to the crux of the question for AI. Is the heightened volume of hardware, infrastructure, and application demand indicative of a new normal? Or a feverish oversupply that will taper over time?

Time will tell, but it seems clear that there are cracks in the narrative arguing in favor of this being a sustainable “new normal.”

Crusoe is a cloud computing company with a mission to “align the future of computing with the future of the planet”. Using a patented Digital Flare Mitigation System, the company captures stranded gas from oil flare sites that would otherwise be wasted and converts it into usable energy to power its data centers. To learn more, read our full memo here and check out some open roles below:

Senior Infrastructure Engineer - San Francisco, CA

Product Manager, Cloud Infrastructure (Network Specialist) - San Francisco, CA

Abridge offers an AI platform that simplifies clinical documentation. Its software listens to provider conversations with patients and summarizes medically relevant information for care teams and patients. To learn more, read our full memo here and check out some open roles below:

Site Reliability Engineer - San Francisco, CA or New York, NY (Onsite or Hybrid)

Full Stack Engineer, Product - San Francisco, CA or New York, NY (Onsite or Hybrid)

Figure AI’s long-term vision is to make labor optional by providing every human on the planet with a personal humanoid robot. To learn more, read our full memo here and check out some open roles below:

DevOps Engineer - San Jose, CA

Senior Full-Stack Engineer - San Jose, CA

Check out some standout roles from this week.

Verkada | San Mateo, CA - Lead Frontend Engineer (Growth), Senior Frontend Engineer (Growth), Solutions Engineer, Senior Backend Engineer (Search)

Moveworks | Mountain View, CA - Senior Software Engineer II (Agentic AI Product), Senior Application Security Engineer II, Senior Software Engineer II (Frontend Infrastructure), Senior Software Engineer (Fullstack)

Hex | San Francisco, CA or New York, NY - AI Engineer, Fullstack AI Product Engineer, Fullstack Engineer

Vercel | Remote (US) - Site Reliability Engineer (Edge), Software Engineer (Platform), Engineering Manager

OpenAI is finalizing a $40 billion funding round led by SoftBank, which would nearly double its valuation to $300 billion and make it the most highly capitalized startup Silicon Valley has ever seen.

OpenAI CEO Sam Altman says the company's GPUs are "melting" due to the high demand for ChatGPT's image generation capabilities, forcing them to temporarily introduce rate limits.

SpaceX’s Fram2 mission will be the first time astronauts orbit over Earth's poles, following a trajectory no human mission has attempted before, providing a "deeper understanding about our planet and its polar regions.”

Rivian's new micromobility startup, Also, plans to leverage Rivian's existing technology and supply chain to offer affordable, high-quality electric bikes and other small EVs for both consumer and commercial use.

Terrestrial Energy, a North Carolina-based nuclear startup, merged with a SPAC to raise $280 million.

Discord is working with Goldman Sachs and JPMorgan to prepare for an IPO as soon as this year.

Frank Slootman, the founder of Snowflake and ServiceNow, joined Cyera's board.

Figure's robots can now walk naturally like humans, after being trained in simulation for just a few hours.

H&M is creating AI clones of 30 models for ads, allowing the models to own and rent their digital twins—even to competing brands.

The Farmer's Dog, a pet food company making personalized, fresh dog food, has surpassed $1 billion in annualized revenue, making it one of the most successful DTC companies currently operating.

Cerebras’ highly anticipated IPO has been further delayed due to a US national security review of a $335 million investment by Abu Dhabi-based G42, which had past ties to China's Huawei.

eToro is going public after previously attempting a SPAC deal, and its IPO timing seems well-aligned with strong crypto trading activity and positive market sentiment for consumer trading platforms like Robinhood.

Google is overhauling its search engine to compete with the rise of ChatGPT in a race to shape the future of the web.

In 2024, VC secondaries surpassed $100 billion in deal volume as startups stayed private longer, tender offers surged, and secondary market discounts narrowed, making secondaries “an essential tool for liquidity” amid scarce IPOs.

StubHub filed to go public on the NYSE after previously exploring a direct listing in 2022 and considering an IPO last summer.

FuriosaAI, a South Korean AI chip startup, reportedly turned down an $800 million acquisition offer from Meta, opting instead to focus on developing its own AI chips.

Taara is a Google X moonshot project that aims to bring fast, affordable, and abundant connectivity to people everywhere using beams of light.

At Contrary Research, we’ve built the best starting place to understand private tech companies. We can't do it alone, nor would we want to. We focus on bringing together a variety of different perspectives.

That's why applications are open for our Research Fellowship. In the past, we've worked with software engineers, product managers, investors, and more. If you're interested in researching and writing about tech companies, apply here!

Great post!